[et_pb_section bb_built="1" fullwidth="off" specialty="off" _builder_version="3.0.89" background_image="https://coeli.com/wp-content/uploads//2018/08/malmo-bro-comp.jpg" parallax="on" module_class="gen-trustee-single-hero"][et_pb_row][et_pb_column type="4_4"][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built="1" fullwidth="off" specialty="off" _builder_version="3.0.89" custom_padding="0px||0px|"][et_pb_row][et_pb_column type="4_4"][/et_pb_column][/et_pb_row][et_pb_row _builder_version="3.0.89" background_position="top_left" background_repeat="repeat" background_size="initial" custom_padding="0px|||" custom_padding_phone="23px|||" custom_padding_last_edited="on|tablet" module_class_2="gen-trustee-single-sidebar" module_class="gen-single-news-content-row "][et_pb_column type="4_4"][et_pb_text admin_label="Tillbaka-knapp" _builder_version="3.0.89" background_layout="light" border_style="solid" custom_margin_tablet="||17px|" custom_margin_last_edited="on|desktop" module_class="gen-back-button hide-in-print" border_style_all="solid"]

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Before making any final investment decisions, please read the prospectus, its Annual Report, and the KIID of the relevant Sub-Fund here

[/et_pb_text][et_pb_text admin_label="Tillbaka-knapp" _builder_version="3.0.89" background_layout="light" border_style="solid" custom_margin_tablet="||17px|" custom_margin_last_edited="on|desktop" module_class="gen-back-button hide-in-print" border_style_all="solid"]

This material is marketing communication

[/et_pb_text][et_pb_text admin_label="Datum / Skriv ut" _builder_version="3.0.89" background_layout="light" border_style="solid" custom_margin_tablet="||17px|" custom_margin_last_edited="on|desktop" module_class="gen-single-news-date-module gen-trustee-print-module hide-in-print" locked="on" border_style_all="solid"]

[blog_post_date]

Print

[/et_pb_text][et_pb_text _builder_version="3.0.89" background_layout="light"]

Monthly Newsletter Coeli Absolute European Equity – July 2022

JULY PERFORMANCE

The fund's value increased 6.3% in July (share class I SEK). The Stoxx600 (broad European index) increased during the same period by 7.6% and HedgeNordic's NHX Equities rose provisionally by 3.9%. The corresponding figures for 2022 are a decrease of 21.8% for the fund, -10.1% for the Stoxx600 and -4.8% for NHX Equities.

EQUITY MARKETS / MACRO ENVIRONMENT

After one of the worst first six months ever, July was the opposite with a strong return on most of the world's stock markets. We came from extremely oversold levels and investors had record cash levels. Only two percent of S&P500 stocks were above their 50-day moving average a month ago, which has happened only five times in the past 20 years. By the end of July, it was clear that the S&P500 had its best July since 1939 with a 9.1% return compared to the broad European index which rose 7.6%. The fund's value increased by 6.3%, more on that later.

The image below shows the returns of various sectors last month. Clear winners were in technology, industrial companies and real estate companies, while the more defensive companies had a more challenging development. Interestingly, among July's five worst stocks in the SXXP600, all (!) were defence stocks: Rheinmetall, SAAB, BAE Systems, Dassault and Leonardo.

Source: Goldman Sachs

Source: Goldman Sachs

A high-octane fuel for technology and growth stocks was the sharp decline in interest rates in July. The American 10-year, which was at levels around 3.50% in June, fell back to around 2.60% The German equivalent was halved in a short time from 1.60% to 0.80%. The sharply falling interest rates, in turn, were due to increasingly clear signals that the economies of various countries are at risk of falling into a recession. The falling interest rates have also put pressure on real interest rates and, for example, the American (10-year) real interest rate is now around zero percent again, see picture below.

After the initial market rebound consolidated, it was time for the Federal Reserve to communicate and update the world on their views on inflation and the economy. As expected, there was a second triple increase of 75 points, but with a slightly softer tone than before. The new message was that they now consider the interest rate to be "neutral" and that in the future it is different economic data that will determine the development of the interest rate. They also removed a forecast about economic developments. The market interpreted this positively, that the worst is behind us, which in turn led to the strongest two-day development after a FED meeting since the 1970s. With a generally low positioning among investors, it is not a bold guess that this "rally" was highly undesirable. The image below shows the development of the US key interest rate so far this year and forecasts for the rest of the year. After that, interest rate cuts are now expected in 2023 (the latest estimate indicates -85 points).

One of the reasons why the FED softened somewhat is signals like the one below which show what the business climate is like for smaller companies in the New York region. Rock bottom, as you can tell, and even slightly worse than during the financial crisis.

Apart from gas, oil and electricity, the vast majority of raw material prices, including wheat, have fallen sharply in recent months, which is very positive.

Below is an excellent graph explaining why the Euro has collapsed against the USD. While Europe has put itself in a really bad place with an unimaginably naive energy policy, the US has had a determination of being self-sufficient. The American gas price has basically not moved in recent years. Painful to watch.

Sweden has also been very good at self-harm, where for more than 20 years they have been unable to increase electricity capacity in southern Sweden. At the same time as six nuclear power reactors were shut down, no new and larger power sources have been added. It will be extremely tough financially for many households (and businesses) this winter and the Swedish power grids communicated and prepared southern Sweden to cut electricity for certain hours this winter! Forecasts indicate that the price of electricity in southern Sweden will be at least twice as high as last winter. As a data point, I can state that our villa accommodation and summer house in December 2021 had electricity bills of a total of SEK 27,000 and it now looks to be doubled (both houses have an air source heat pump). In that case, it means that you have to have a gross salary of SEK 100,000 just to pay the upcoming electricity bill in December.

Good job above all by the Social Democrats and the Green Party who shut down Oskarshamn 2 (2015), Oskarshamn 3 (2017), Ringhals 2 (2019) and Ringhals 1 (2020). At the same time, our Environment Minister, Annika Strandhäll, thought in an interview on SVT that two nuclear power plants were shut down and three were in operation (the correct answer is six and six respectively). Sweden's energy policy is like a nightmare and it will last for many years. In practice, it is like an extra tax because we had incompetent politicians who, in exchange for government power, overturned an exceptionally well-functioning energy supply.

Source: Steget efter

Source: Steget efter

We top the above with the latest GDP forecasts for Europe published by the European Commission last week. Sweden is expected to have the lowest economic development in the entire EU in 2022 and the picture for 2023e unfortunately looks exactly the same - Sweden is last!

Source: EU Commission

Source: EU Commission

Italian Prime Minister, Mario Draghi, tendered his resignation during the month causing Italian credit spreads to widen significantly. The combination of a highly indebted country (135 % of GDP) and the EU's third largest economy is not brilliant and since last autumn the interest rate in Italy has risen from around +0.5% to just over 3% (the highest level of around 4% was reached when Draghi announced his departure). The sharp rise prompted the ECB to search its toolbox and construct a new solution – TPI. The Transmission Protection Instrument will enable the ECB to buy bonds in countries that it perceives have had or are experiencing a significant and unwanted deterioration of financial conditions.

In the end, even Boris Johnson could not withstand the pressure from the public and his own ranks. Our monthly newsletters will be a tad boring as the constant scandals will now probably disappear, but for the world and not least Europe, it is a blessing that Boris is stepping down as Prime Minister of Great Britain. On the same day he resigned, the British pound strengthened significantly, which says a lot. In his closing speech, he gave a number of pieces of advice to his successor: "Keep us close to the Americans, stand up for the Ukrainians, stand up for freedom and democracy everywhere and cut taxes and deregulate wherever possible." His last words in Parliament were – “Hasta la vista, baby”

Long positionsTruecaller

During the month, Truecaller released yet another report that exceeded expectations. Perhaps the numbers speak for themselves:

- Sales increased by 100% compared to the previous year

- The operating margin amounted to 44% and operating profit rose by 163%

- The number of monthly and daily users rose by 15% and 17%, respectively

- As of the last quarter, Truecaller had roughly 320 million monthly users

With a low-capital business model the cash flow follows nicely and most of the profit turns into cash on the balance sheet.

Operationally, most things are going Truecaller's way right now. The company continues to release new features and products, which has increased user engagement (measured as the number of monthly users who are also daily users). The geographical diversification continues even though India will be the company's largest market for a long time. We are impressed by Truecaller's latest business division, Truecaller for Business, which basically went from zero revenue at the start of 2020, to an estimated turnover just above SEK 100 million in 2022.

Even though business is going very well, the share has had a 2022 with peaks and valleys against the background of the year's opening "tech-freak", placements and a couple of critical articles in the Indian press (which we covered in previous monthly newsletters). It should also be said that the share price was high at the start of the year. After the report for the second quarter of 2022, the market chose to reward the stock significantly for the first time. The price increase for July landed at 61%. The price rise from the IPO last year to the end of July was approximately 52%. Truecaller was the fund's strongest contributor in July with a positive impact of approximately 2.50%.

Lindab

The Lindab share has had a tough time this year against the backdrop of general economic fears (and a high valuation at the start of the year). Although the first half of 2022 is now history, there is little in those reports to suggest a slowdown. CEO, Ola Ringdahl, also believes in stable demand during the remaining part of 2022. The big question is rather what the demand will look like in 2023–2024.

Although Lindab is not immune to recession, there are several mitigating factors:

- The company has a large exposure to renovation projects, which are typically less affected by recessions.

- Lindab's large investment program has only been half implemented, and will continue to contribute to profitability improvements regardless of the state of the economy for several years to come.

- Europe's energy crisis will most likely increase the demand for energy-efficient ventilation. In this area, Lindab has launched products with a quick payback period for the end customer and which can be easily installed in already existing ventilation systems.

- Lindab should be able to gain market share in a worse economic climate (as proven during the pandemic).

- The stock is trading today at single-digit earnings multiples on our estimates, which suggests that the market has already priced in some concerns in advance (given that our estimates are reasonably correct).

Many are also worried about the impact a falling steel price will have on sales, which have been very positively affected by price increases in recent quarters. We do not believe that Lindab will lower prices with a 1:1 relationship to the steel price because the company, among other things, continues to see large cost inflation in other areas (transport/logistics, energy, wages, etc.). That will have to be compensated by means of price adjustments.

All in all, we have a positive view on Lindab's prospects even in a tougher economic climate. We believe that today's valuation is pricing in too much forecasted troubles. After another good report (beating expectations by around 4%), the stock rose 19% in July and was the fund's third strongest contributor with a positive impact of around 1%.

SLP

It was a strong month for the SLP share, which recorded an increase of 31%. The report for the second quarter came in above expectations but without any major surprises. Despite a very challenging market, the company made acquisitions for SEK 0.5 billion during the first half of the year and the net asset value per share rose by 58% compared to the same period last year. Most of the transactions are off-market or via sales-lease-back, which allows SLP to buy at superior prices to the market. The company delivers fully in line with our expectations and we continue to like the stock, which is valued at just over P/E 19x 2023e. The stock has risen 24% since we invested in the IPO. SLP was the fund's second strongest contributor in July with a positive impact of approx. 1.2%.

ISS

The ISS share had a good month with a price increase of 13%, which brings the full-year figure to just over 1%. During the month, several companies in the sector (Compass Group, Elior, Sodexo, Coor, etc.) reported overall good numbers. It has likely spilled over to the ISS share. We also note that a company like Securitas, which is also characterized by being a very staff-intensive business, has managed to dodge wage inflation nicely so far. We believe that the concern over salary inflation for ISS is exaggerated. Whether we get it right remains to be seen. The next report will be in August.

Wincanton

The British logistics company came up with another positive update in July. The influx of new customer contracts continues and the company has succeeded well in compensating for inflation. Under its new management, Wincanton has succeeded in turning the business around in an impressive manner. However, the valuation has not yet adjusted in our favor, even though the investment has been okay so far (the stock has advanced about five percentage points since our initial investment). We believe that it is only a matter of time before the revaluation comes. Logistics companies are often highly valued on the stock exchange, and Wincanton's business is increasingly directed towards customers who operate in structurally growing markets. The stock rose 9% in July.

Teleperformance

France's Teleperformance, which mainly deals with the outsourcing of customer support and related services, reported a fine result for the first half of the year in July. There are still no clear signs of a slowdown in their business. On the contrary, Teleperformance has historically been successful in winning new contracts during recessions when their customers can save money by outsourcing their customer service to them. The stock rose 11% in July.

Tate & Lyle

Our investment in Tate & Lyle has been one of the best of the year, having risen by around 26% (31 percentage points better than the European index) since we invested around six months ago. The main points of our investment thesis can be read in our February newsletter. So far, the whole thing has played out roughly as we thought: after the divestment of 50% of the company's less valuable segment, Primary Products, there has been an increase in valuation as Tate & Lyle has been able to more clearly highlight good results in the golden product segment, Food & Beverage. The rise for the month of July landed at 7%.

Rejuveron

As previously described, since December 2019 we have had an unlisted holding in Swiss Rejuveron which is a biotech company. In April, a new capitalization round was carried out where the valuation increased from CHF 30 to CHF 120 per share. The company has had a good operational development this year, but in view of the sharp decline in the stock market during May and June (even though, as you know, it rose in July), we have chosen to write down the valuation by 15%. The fund's value development in July was affected by approximately -0.7% because of this. The company aims for a stock market listing in 2023.

Biovica

Saturday the 30

th of July, Biovica also took the opportunity to deliver long-awaited news. Their product DiviTum received FDA approval (510(k)) and thus the US is opened up for sale and clinical use of the product. The decision was delayed for over a year as a result of Covid-19 priorities at the FDA and specific issues surrounding DiviTum. The company already has an organization in place in the US and is now ready to launch the product before the end of the year. This is the biggest thing that has happened in the company's history and we are happy to have been involved in making this journey possible.

Short positions

The short portfolio contributed negatively during the month. Our short positions on a Swedish small-cap index had the biggest negative contribution together with our positions on the German DAX. A couple of stock specific short positions that contributed positively to the result were German Adidas and Swedish SCA.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning of the month was 52% and 68% respectively.

Summary

We finally got to experience a strong equity month. Our companies' earnings in the second quarter made us and other investors happy and we saw a stock market that, unlike earlier this year, behaved more rationally. There was still some volatility, but significantly less than before and it was easier to understand different price movements. What was also pleasing was that the breadth of the market, the number of stocks that rose, increased which indicates that this upturn is of higher quality than the others we saw during the spring.

A month ago, participation in the stock market was at a record low due to record pessimism. One swallow doesn't make a summer, but anyone who has studied the historical pattern could conclude that when the bow is so tight, it doesn't take much for share prices to rebound upwards. That's how it happened this time too, and we got to experience the strongest July in over 80 years. For those of you who like statistics: in the months when the stock market rose by more than 9%(based on roughly 80 years of history), the development six months later was +12.3% and twelve months later +17.6%.

The quarterly reports for the second quarter of 2022 have in many cases been surprisingly good, not least regarding the outlook for the second half of the year. Below shows how the companies within the Stoxx600 delivered in relation to the market's expectations. The best sector/industry was mining companies, which beat expectations in 78% of the cases, while real estate companies were the worst sector. The picture is as of the end of July/August, so a small percentage of companies are missing.

Goldman Sachs' risk monitor shows a continued cautious positioning even if the most extreme levels of a month ago are in the past.

The risk premium is still at high levels (10.9 on July 29), which is higher than the average for the last 11 years. This implicitly means, with an assumption that the risk premium should go towards the historical average, that the profit estimate should be reduced by 8%. Note the sky-high risk premia in auto, financial and energy stocks and thus the implied downward revisions to earnings discounted into its share prices.

Source: Kepler Chevreux

Source: Kepler Chevreux

Valuations in Europe are at historic lows with a modest P/E of 12x trailing 12 month earnings. However, it is not the valuation that is the problem right now, but only how much the companies' earnings should decrease.

Source: Goldman Sachs

Source: Goldman Sachs

Values for different regions currently look like below. There is still a very large difference between Europe and the USA.

Source: Goldman Sachs

Source: Goldman Sachs

The following illustrates how value stocks have developed in relation to cyclical sectors over the past 20 years. The development goes in waves and is reasonably in sync with the economic development. The relative excess return for defensive stocks this year is significant and it is likely that the trend will turn around sometime this fall (our view).

As previously communicated, we assess that we are around the highest levels for inflation and thus also for the interest rate. A sharp fall in interest rates in July boosted growth stocks while value stocks lost relatively, see graph below. We also came off extremely depressed levels and not since the Lehman crash has the Nasdaq been below its 100-day moving average for such a long period.

The PE number for the highest valued companies in Europe a year ago compared to today. Interesting that there are many Nordic companies on the list. The fund has had a short position in Vestas for an extended period.

Source: Kepler Cheuvreux

Source: Kepler Cheuvreux

The takeovers continue and today, when this is being written on August 3rd, Italian Tod's, for example, has received an offer. In Sweden, Swedish Match, Leo Vegas, Haldex and Cary Group have received takeover offers in recent months. The venture capital companies still have enormous amounts of capital to put to work, see below. Our feeling is that the activity of these actors has been tentative in recent months, but we guess that it will pick up again after the summer.

Source:Goldman Sachs

Source:Goldman Sachs

The repurchase mandate starts again after the reporting season and 2022 will be another record year.

Source: Goldman Sachs

Source: Goldman Sachs

In summary, we maintain our view that the market is trading within a range. A month ago we were in the lower range and now in the higher range. There are many indicators that look better than a month ago and the companies have in many cases impressed the market, but we are probably not yet on safe ground. Our best assessment is that the next FED meeting in September will determine much of the development during the autumn. The chances that we can break out of the current trading range after that are relatively good.

What could continue to drive share prices up in the coming weeks are:

- Continued careful positioning in the starting position

- Expected large purchases of shares from systematic macro strategy funds and quant funds in coming weeks (JPM estimate)

- The share of short equity positions remains at the highest levels in two years

- Big buy-back programs will start rolling again

- A certain risk appetite has returned

What speaks against continued uptrend is that the rise has been unusually strong. In addition, we continue to have very large geopolitical problems. We are also approaching September, which is typically the worst month of the year, see picture below.

Source: Top Down Charts

Source: Top Down Charts

As you know, we do not spend our working days trying to find the bottom and the top in the market, but invest in the companies we believe have the right circumstances to create significant value for their owners in combination with an attractive price of the share. Those are the only two components required to create excess returns over time. Finally, we can also announce that at the turn of the month we started our new mandate that we told you about last month. There are clear overlaps in terms of holdings and of course strategy and we would like to thank everyone involved at Coeli for a flawless delivery!

Mikael & Team

Malmö on 8 August 2022

[/et_pb_text][et_pb_post_title _builder_version="3.0.89" title="on" meta="off" author="off" date="off" categories="off" comments="off" featured_image="off" featured_placement="below" text_color="dark" text_background="off" border_style="solid" module_class="gen-single-news-heading-module gen-trustee-single-headline" date_format="d M, Y" border_style_all="solid" disabled_on="on|on|on" disabled="on" /][et_pb_text admin_label="Coeli Nordic Corporate Bond Fund R-SEK" _builder_version="3.0.89" background_layout="light" module_class="gen-table-module" disabled_on="on|on|on" disabled="on"]

Coeli Nordic Corporate Bond Fund

| Performance in Share Class Currency | 1 Mth | YTD | 3 yrs | Since incep |

| Coeli Nordic Corporate Bond Fund - R SEK | 1.30% | -0.93% | 3.38% | 14.52% |

| | | | |

[/et_pb_text][et_pb_text admin_label="Coeli Nordic Corporate Bond Fund R-SEK" _builder_version="3.0.89" background_layout="light" module_class="gen-table-module" disabled_on="on|on|on" disabled="on"]

[cg_linear_graph id="31122"]

[/et_pb_text][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads//2020/10/ncbr.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" disabled_on="on|on|on" disabled="on" /][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads/2019/01/Gustav-Fransson6.jpg" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" custom_margin="||21px|" disabled_on="on|on|on" disabled="on" /][et_pb_text admin_label="Namn och title" _builder_version="3.0.89" background_layout="light" module_class="gen-single-ingress-module" custom_margin="||40px|" disabled_on="on|on|on" disabled="on"]

Gustav Fransson

Portfolio Manager of Coeli Nordic Corporate Bond Fund

[/et_pb_text][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads/2018/10/Alexander-Larsson-Vahlman.jpg" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" custom_margin="||21px|" disabled_on="on|on|on" disabled="on" /][et_pb_text admin_label="Namn och title" _builder_version="3.0.89" background_layout="light" module_class="gen-single-ingress-module" custom_margin="||40px|" disabled_on="on|on|on" disabled="on"]

Alexander Wahlman

Senior Analyst

[/et_pb_text][et_pb_text admin_label="Top Holdings (%)" _builder_version="3.0.89" background_layout="light" custom_margin="||20px|" module_class="gen-trustee-single-table" disabled_on="on|on|on" disabled="on"]

Top Holdings (%)

| LANSBK 1.25% 18-17.09.25 | 4.1% |

| NORDEA HYP 1.0% 19-17.09.25 | 4.1% |

| SWEDBK 1.0% 19-18.06.25 | 4.1% |

| WHITE MOUNT FRN 17-22.09.47 | 3.9% |

| B2 HOLDING FRN 19-28.05.24 | 2.9% |

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row _builder_version="3.0.89" background_position="top_left" background_repeat="repeat" background_size="initial" module_class="gen-single-news-content-row gen-trustee-single-content-row" custom_padding="0px|||" custom_padding_phone="23px|||" custom_padding_last_edited="on|tablet" module_class_2="gen-trustee-single-sidebar" disabled_on="on|on|on" disabled="on"][et_pb_column type="2_3"][et_pb_text admin_label="Tillbaka-knapp" _builder_version="3.0.89" background_layout="light" border_style="solid" custom_margin_tablet="||17px|" custom_margin_last_edited="on|desktop" module_class="gen-back-button hide-in-print" border_style_all="solid"]

Note that the information below describes the share class (I SEK), which is a share class reserved for institutional investors. Investments in other share classes generally have other conditions regarding, among other things, fees, which affects the share class' return. The information below regarding returns therefore differs from the returns in other share classes.

Return to Fund page

[/et_pb_text][et_pb_text admin_label="Datum / Skriv ut" _builder_version="3.0.89" background_layout="light" border_style="solid" custom_margin_tablet="||17px|" custom_margin_last_edited="on|desktop" module_class="gen-single-news-date-module gen-trustee-print-module hide-in-print" locked="on" border_style_all="solid"]

[blog_post_date]

Print

[/et_pb_text][et_pb_post_title _builder_version="3.0.89" title="on" meta="off" author="off" date="off" categories="off" comments="off" featured_image="off" featured_placement="below" text_color="dark" text_background="off" border_style="solid" module_class="gen-single-news-heading-module gen-trustee-single-headline" date_format="d M, Y" border_style_all="solid" /][et_pb_text _builder_version="3.0.89" background_layout="light"]

Utveckling september

Fondens värde sjönk -5,1 procent i september (andelsklass I SEK). Stoxx600 (brett Europaindex) sjönk under samma period med -3,4 procent och HedgeNordics NHX Equities var preliminärt oförändrat. Motsvarande siffror för 2021 är en ökning om +21,6 procent för fonden, +14,0 procent för Stoxx600 och +6,4 procent för NHX Equities.

Equity markets / Macro environment

After seven consecutive months of positive performance the world’s stock markets were poised for some degree of turbulence. Volatility was especially high in some equities and on Monday, September 20, the highest nominal volume ever traded was reached in options on the S&P500 (!) The broad European index fell by 3.4 percent in September compared to the S&P500 which fell by 4.8 percent. The fund also had its first negative performance since October last year with a decline of 5,1 percent. More about that later.

Despite high levels for many stock indices, sentiment among investors has been relatively gloomy. Bank of America's monthly survey recently showed that only 13 percent of managers expect a positive market in the future, which is the lowest figure since April 2020 (and that was clearly wrong). The reasons cited are China's growth problems, the crisis-stricken Chinese real estate giant Evergrande, the development of the delta variant, declining profit growth and, of course, rising inflation. However, they are still overweight equities which is perhaps not so strange when you have to pay to lend your capital to countries. As interest rates rose at the end of the month, the German 10-year interest rate followed with a giant step from - 0.25 percent to - 0.17 percent… The picture below is an overall risk indicator, and we are around zero (neutral).

The news flow in September began with record high inflation figures in Europe at +3.0 which exceeded market expectations. The corresponding figure in July was + 2.2 percent. It was the fastest growth rate since November 2011 and several countries recorded up to five percent in inflation rate. The pressure on the ECB to reduce its support measures is increasing. On Friday, October 1, new inflation figures came in for September, which showed a further acceleration in the inflation rate by +3.4 per cent.

The rate of change can be mostly attributed to rising energy prices that are starting to create real problems in the world's economies as well as agricultural shifts. The picture below shows that food prices are at record high levels over the past 60 years. The biggest losers are the poorest part of the population.

In the slightly longer term it is forecasted that it is not excessive demand that will drive inflation, but rather a limited supply, and then both in terms of products and labour. At the end of September, long queues were reported at petrol stations across the UK when fuel ran out and there were not enough truck drivers to refuel. Prime Minister Boris Johnson urges his citizens to refuel sensibly and at a normal rate. You wanted Brexit, so there you go. In sheer desperation, Johnson has now issued 5,000 temporary short-term visas for temporary drivers. Good luck.

M25 spring 2022?

Below are European gas prices which have risen in a seemingly uncontrolled fashion and recorded the highest September prices ever. A silent prayer for the mild winter. We guess that this development will soon be a major topic in the media, and it will undoubtedly create various problems and somewhat reduce next year's expected growth. It feels reassuring that Per Bolund (Swedish Green Party MP) claims that there is no electricity shortage in Sweden because then the costs for ordinary people would be unbearably high during the winter (which of course they will be). Rising gas and electricity prices have led European politicians to start discussing billion-dollar subsidies (in euros) to households and manufacturers who will experience sharply rising electricity bills over the winter.

Source: Bloomberg

Henrik Svensson, site manager at the oil-fired power plant in Karlshamn (south Sweden), does not agree with Per Bolund that we have a surplus of electricity in the country. For large parts of September, the power plant ran at full capacity and burned 240k liters of oil per hour. Henrik Svensson believes that it is electricity shortages and high electricity prices that are behind the high production. He also says that there is a lack of planned power production in southern Sweden and that it will take many years before the electricity grid is strengthened and new electricity production is in place. Sweden today burns more oil than we have done in 10 years. A gigantic energy policy and climate policy failure signed by the Green Party.

Source: Steget efter

Winning candidate for this year's Christmas presents below.

The change in the US 10-year interest rate created considerable pressure on, primarily, growth stocks at the end of the month. The performance dispersion for different sectors was very large in September with oil shares as a clear winner. This was also felt in the last days of September.

Source: Bloomberg

Below is the development for the US 10-year interest rate. The turbulence in the stock market was caused by the change in interest rate level breaking through on the upside, as can be seen in the chart.

There have been countless attempts to explain the turbulence in recent weeks. The recent and significant amount of options being exercised, Evergrande, interventions by the Chinese government, Fed tapering, Bank of England expected to raise interest rates, delta variant, inflation, bottlenecks in production, difficulties in finding staff, rising energy prices and declining growth rates. We think it is enough to look at the picture below. Rising interest rates hit hard at growth companies' valuations.

Goodbye Mutti and thank you for an extraordinary effort for Europe!

Source: Nyhetsbyrån TT

She was politically in a class of her own during the euro crisis ten years ago and Sweden also has her to thank for a lot. Despite a somewhat weaker performance in recent years, German citizens have experienced significantly better economic development than many others.

On September 29, the covid-19 restrictions in Sweden were finally removed and we can now, in principle, start living a normal life again. The number of bookings for winter holidays skyrocketed to the great joy of the tourist and transport industry. In recent months, tourism activity in the Mediterranean has been "extraordinary" and much better than forecasted before the summer. Luxury travel is also reaching new heights. Private jet passengers to Mallorca increased by +70 percent in July compared to July 2019 with an average of 83 private jets per day landing in Palma. If you want to rent a yacht, you are being referred to next year as basically everything has already been fully booked.

We now belong to a minority group. Passively managed capital exceeds actively managed capital for the first time ever. This will give us more opportunities as mispricing increases.

In addition to being one of the world's best stock markets this year, Sweden also has the most listed companies in the entire EU. Bloomberg drew attention to the fact that there are now around 1,000 listed companies on the various trading platforms in Stockholm. More than 80 percent are smaller companies, and the list is filled with new listings every day until Christmas! For us, it is interesting as we are constantly looking for new potential core holdings. In recent weeks, we have identified one which we write about under Long Positions.

We end this section with a picture that well reflects today's political level.

Source: Kluddniklas

Long positions

Truecaller

During September, we did a lot of work on the Swedish company Truecaller which will go public on October 8th. Truecaller is one of the most interesting companies we’ve seen in recent years. Truecaller has developed a phone application that can, among other things, identify unwanted calls from, for example, telemarketers. The app is one of the top ten most downloaded applications globally, and in some of the main markets such as India, Nigeria and Indonesia, it is one of the three most downloaded apps. As a Swedish company with headquarters in Stockholm, the firm has chosen to list on the Swedish stock exchange, which we are very happy about.

Truecaller was founded in 2009 by Alan Mamedi and Nami Zarringhalam. They met at the Royal Technical University in Stockholm, and they continue to be active in the company as the CEO and Chief Strategic Officer (CSO), respectively. When they released the first version of the app, they received 10,000 downloads within one week. By 2013 they had reached over 10 million users globally and in Q2 2021 they had reached 278 million monthly users. Throughout their journey, Truecaller has attracted several well-known investors such as Sequoia Capital (early investors in Apple, Whatsapp, and Zoom among others), Atomica (Skype-founder Niklas Zennström’s investment company), and Kleiner Perkins (early investors in Google, Amazon, and Spotify among others).

Until recently, revenue streams have mainly consisted of income from in-app advertising. In addition to this, there is a premium version where paying users can get additional functionalities. That business accounted for around 20 percent of revenues in 2020. During the fall of 2020, Truecaller launched a corresponding offering that targets corporates. This part of the business allows B2B customers to be listed as verified callers when they call private people. It can for example be a security company that calls about an alarm or a courier company that needs to get in contact with a receiving customer. It is a common problem that these types of companies get rejected when the call-receiver doesn’t recognize the number.

Truecaller declares that their product benefits from network effects. i.e., the product gets better the more people who use it (think Facebook). This can be relatively easy to appreciate since phone number identification inherently evolves from reporting of unwanted calls by the users, i.e., when enough people have reported an unwanted call Truecaller flags for this in the app). Over time, Truecaller has built a database containing 5.7 billion unique phone-identities. Network effects doesn’t just build a better product over time, they also increase the entry-barriers for potential competition.

The majority of Truecaller’s income comes from developing countries. The company explains that the problems related to spam emails, harassment, unwanted calls, and messages are more common there than in the western world. India is Truecaller’s largest market where these types of problems are significant. One positive aspect of the geographical exposure is that it allows for a nice structural tailwind: the population growth in developed markets is much higher than in the west (driven by an increasing average age) and the smartphone penetration is growing fast.

Historically, 97 percent of all app downloads have been organic. However, management has begun to experiment with user acquisitions by the way of advertisements through, for example, Facebook. The returns on user acquisition looks extremely attractive. In some markets, such as India, Truecaller could achieve a return on investment of up to 20x on every spent dollar. In more mature markets, such as the USA, the same multiple amounts to 4x, still very attractive. Indonesia, which is a relatively new market to the company, has a multiple of 0.8x. This means any user acquisition spend in Indonesia is unprofitable at this point. However, management is confident that the return profile will wander above the 1x as more users join and the network effects take place. In summary, the investment opportunities are plentiful and attractive – and unique.

In summary, several things speak for significant growth in the future. The investment in paid user acquisition, a sharpened premium-offer, the newly launched B2B product and continued growth of the advertising business. In addition to this, acquisitions may likely follow.

Growth has been prioritized over profitability and it is only recently that the company began to report profits. In 2019 sales grew by 57 percent. In 2020 the corresponding figure was 64 percent, and during the first half of 2021 the company’s sales grew with as much as 151 percent in comparison to the same period last year (which was partly affected by the pandemic). During the first half of this year, the company’s operating margin was 32 percent. As you can imagine, Truecaller is very capital-efficient. Working capital is very low which gives a nice cash conversion and a very high return on capital employed – all attributes that are required to create a very successful and valuable company over time.

Truecaller targets a revenue growth of at least 45 percent between 2021-2024e. After 2024 the EBITDA-margin should be at least 35 percent. The sum of the year-on-year growth and the EBITDA-margin should amount to at least 70 percent (a variant of the rule of 40 that tries to balance growth and profitability). We don’t think it will be difficult to reach these targets and the analyst estimates we have looked at are cautious, especially regarding profitability. In our preliminary prognosis for 2023, our EBITDA-estimate is around 16 percent ahead of the analyst estimates that we’ve studied. This is based on that Truecaller can continue to grow sales much faster than hiring new people while the gross margin improves slightly in coming years.

The gross margin is an interesting aspect of the equity story. Truecaller’s gross margin amounts to approximately 70 percent. Most of the cost of sales consists of platform fees to Apple and Google. Since Apple and Google practically control the distribution channels for apps together, a duopoly has occurred and prices for app-developers such as Truecaller have remained high around 25-30 percent of sales. This situation is now heavily criticized from all parts of the world since the situation is not considered competitive, for example

look at this analysis about an American court ruling concerning a twist between Epic Games and Apple. We believe Google and Apple’s fees will decrease over time – which would be a positive event for Truecaller. Furthermore, Truecaller’s new business deal bypasses Goggle and Apple, which gives a gross margin of close to 100 percent. This will strengthen the profitability even more.

There are of course risks associated with the dependence on Google/Apple (which is the case for every company in the application business); the geographical exposure and one should never write off the threat of competition even if it seems far away at this stage. However, we do believe the benefits outweighs the negatives. Truecaller has excellent financial characteristics, operational founders with large shareholdings who will remain active in the business and some of the world’s most well-known investors behind it. We therefore look forward to being included as an anchor investor ahead of the stock exchange listing on October 8th. We are even more excited to follow the company’s successes in current and new markets in the coming years.

CVS Group

One of the happiest days of the month was when our veterinarian company CVS Group released their interim numbers. Once again, the company beat analysts’ expectations which have been raised several times over the course of the year. In the first two months of the new financial year (which begins in July), the company has grown by 17 percent. This can be compared with the growth expectations for the full year which, before the report release, were 7 percent. Once again, analysts have thus far been “forced” to upgrade their assumptions. In a sour September stock market, the share fell 3 percent.

It becomes clear that the positive effect of the pandemic on pet ownership is more tenacious than ever. Pets live for many years, and we believe many underestimated the importance of the large number of new customers during the pandemic. Below is a graph of Google searches for veterinarians in the UK as well as data from the Swedish Board of Agriculture regarding the number of newly registered dogs. We speculate that the UK has similar trends as Sweden. The data points are also positive for our other pet company Swedencare. Pet companies are obviously still hot; right now there’s a bidding war going on over the German pet company Zooplus, where EQT is currently in the lead with the highest bid. We also note that there have been several venture capital-led acquisitions of veterinary companies at higher multiples than CVS is valued at.

Source: Jordbruksverket, Coeli

Source: Google Trends, Coeli

Lindab

Since our first investments in Lindab in the autumn of 2019, the thesis has always been that the building systems business segment did not fit into the business and in September, management finally found a buyer for the company. The transaction entails a write-down of goodwill corresponding to SEK 430 million, but it is cash flow neutral. Lindab took the opportunity to update its financial targets; the company now wants to grow by 10 percent per year (of which approximately two thirds are through acquisitions) and reach an operating margin of at least 10 percent (previously 10 percent over a business cycle). The share responded positively to the message.

We noted broad insider purchases in Lindab during the month, also from CEO Ola Ringdahl himself, which we think bodes well for the report in October. Despite this the share price decreased 8 percent in September.

Victoria

We have written several times about the British flooring company Victoria, which in September had a weak share price development of 17 percent. By all accounts, the company is doing well – during the month it was reported that sales rose 70 percent compared to 2020, and 50 percent compared to 2019. If you only partially extrapolate these figures for the rest of the year, it is obvious that analysts’ expectations are too low. We believe that this month’s decline is related to flows: growth companies and small and mid-cap companies were some of the most affected sectors in September – Victoria was hit from both sides. We have increased our position in recent days.

The Pebble Group

One of the month’s (few) joys was Pebble Group. As we previously wrote, the company is active in the market for gift advertising, i.e. gifts that companies give to customers, employees, and other stakeholders for marketing purposes. In September the company came out with its half-year figures that were better than expected. Pebble’s software division, Facilisgroup, is growing better than our expectations. This is also the part we believe the market is valuing too low. The stock rose 10 percent in September.

Knaus Tabbert

During the last trading day in September, our German motorhome manufacturer Knaus Tabbert announced that the forecasts for 2021 must be lowered due to component shortages. We are not particularly surprised that this has happened given what we have seen from other vehicle manufacturers. If the company can remedy these supplier problems, management believes that 2022 will be unaffected at best, as Knaus still has a bursting order book, increased production capacity and more suppliers from January next year. The share fell 7 percent in September.

Short positions

The short portfolio contributed with a negative result during the month. Our short-term negative positions in the German DAX had the largest negative contribution. Some stock specific short positions that contributed positively to the result were Swedish Dometic, German Henkel and Norwegian NEL.

Exposure

The net exposure, adjusted for our unlisted holdings, at the beginning and end of the month was 76 and 74 percent, respectively.

Summary

September's negative return of x percent also meant the end of the fund's, so far, longest period of positive return (10 months). We are obviously disappointed with that, but we have been in the game long enough to understand that equities sometimes must fall to be able to refuel and continue their upward trajectory. In general, September was the weakest month for many equities since the crisis started 1.5 years ago. September, otherwise, started strong for us and was a continuation of an unusually good performance at the end of August. Our companies presented many good news (except for Knaus Tabbert on the last day of the month) but small-caps and especially those categorized as growth shares, had a very weak performance during September. The main reason for this was, as previously mentioned, the change in the US long-term interest rate and general "risk off".

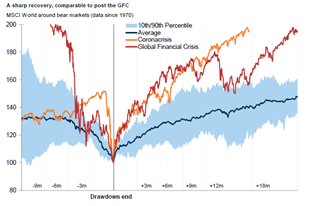

The picture below shows the development since March last year compared with the corresponding time intervals in the financial crisis in 2009 and onwards. Both periods have shown an unusually strong recovery and the current trend is even stronger than when the financial crisis raged 12 years ago.

Source: Goldman Sachs

Since the crisis started 1.5 years ago, we have had three different phases. The first and shortest, "despair", showed a decline in prices of 33 percent. The second phase, "hope", ended at the beginning of this year and showed a very strong return of 79 percent despite declining earnings. The last, “growth”, where we are now, has shown +11 percent in share prices with sharply rising growth for companies' earnings, but at lower valuations.

Source: Goldman Sachs

The recovery for American companies (below) has been extremely strong and compared to 2019, the 2021 profits will be approximately 36 percent higher. Very impressive.

Source: Goldman Sachs

It is very gratifying that Europe, for once, is keeping up with the United States and showing strong profit growth. Compare this with the non-existent profit growth between 2007–2019 (!)

Despite rising equity prices, valuations have fallen and Europe is now trading around 16x the profit 12 months ahead. It's not very strenuous (we think). For an average commercial property, you can get a return of maybe 3 percent before net financial costs. After financing, this corresponds to at least P/E 50x. And paying to lend to different countries does not feel like an exciting alternative either.

Source: Goldman Sachs

The valuation of global shares in relation to global GDP looks more strained. A major reason for this is the central banks' aggressive policy.

The valuation of the major leading technology companies is at an average level seen from the last five years.

Source: Goldman Sachs

The image below is striking. It shows that Swedish property prices, which have risen by almost 200 percent over the past 15 years, have had the same development as the money supply. In theory, price per m2 and krona is unchanged for the past 15 years. Is there anyone who still doubts that the world's central banks are responsible for the largest wealth creation in human history? It is important to be on the wagon because when it is gone you’ve missed it. And what central banks cannot push, the price of bitcoin for example, rises even more as central banks cannot make more of it. The opportunities for central banks to reverse the band are few. In the long run, this means that the next 10 years will, overall, be a good period for, for example, stock picking. All forms of uniqueness (growth) will be highly valued to compensate for the fact that the value of money decreases at a rapid pace.

If there is anyone who is still not convinced, take a look at the picture below. The market capitalization of the S&P500 divided by the Fed's balance sheet….

Source: Bloomberg

Onwards and upwards. The wealth of American households is accelerating away from the change in GDP.

Thank you Fed and all the world central banks!

Citigroup's surprise index has weighed down and analysts' profit estimates are also starting to soften. Not a good combination and it has undoubtedly contributed to the weak development in the stock markets recently.

It took a full 219 days for the S&P500 to have a decline of 5 percent. We will see how high the next bar will be.

Timing is everything. A fascinating graph that shows the importance of having reasonable timing in decisions.

Source: Goldman Sachs

Despite a difficult month behind us, it feels reasonable to expect a stronger market during the last quarter of the year. Our view is that we are still in a rising market, although we are likely to experience some turbulence for a few more weeks. "Bear markets" are constantly declining with sharp rallies while "bull markets" continue to rise with some strong drawdowns. We therefore believe that we are still in a rising market.

Some statistics to cheer you up. The S&P500 managed to rise by 0.2 percent in the third quarter (Europe -1.9 percent) which means six consecutive positive quarters. This has only happened eight times before and only on one of the (eight) occasions has the following quarter yielded a negative return. Two quarters later, it has in all cases yielded a positive return. In addition, for the past 20 years, October has been the fourth best month, thus much better than its reputation. Having pointed that out, October takes first place in terms of most frequent daily movements that exceed one percent.

The Stockholm Stock Exchange, which is an excellent reference point, had risen by 30 percent at its highest about a month ago, but is currently at 20 percent. Even more important is that measured in USD, OMX has "only" risen by 13 percent, which is in line with the US stock markets. This is hardly excessive given the profit growth among the companies. The risk premium in the market is high.

Investors are reasonably careless, and we are approaching the turn of the year. Global growth is well above average and interest rates are extremely low. Given how cruel the market has been to many investors this year, with sector rotations and a high concentration of companies driving performance, it almost feels obvious that the broad mass of investors will continue to reduce risk in their portfolios and then be short equities at year-end when the market rises. We'll see, but that's our main scenario right now.

We are now closing the books for the third quarter, and we look forward to the end of the year and above all the entrance for Truecaller on the Stockholm Stock Exchange on October 8!

Thank you for this month and we'll hear from you later.

Mikael & Team

Malmö on 5 October

[/et_pb_text][et_pb_text admin_label="Coeli Nordic Corporate Bond Fund R-SEK" _builder_version="3.0.89" background_layout="light" module_class="gen-table-module" disabled_on="on|on|on" disabled="on"]

Coeli Nordic Corporate Bond Fund

| Performance in Share Class Currency | 1 Mth | YTD | 3 yrs | Since incep |

| Coeli Nordic Corporate Bond Fund - R SEK | 1.30% | -0.93% | 3.38% | 14.52% |

| | | | |

[/et_pb_text][et_pb_text admin_label="Coeli Nordic Corporate Bond Fund R-SEK" _builder_version="3.0.89" background_layout="light" module_class="gen-table-module" disabled_on="on|on|on" disabled="on"]

[cg_linear_graph id="31122"]

[/et_pb_text][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads//2020/10/ncbr.png" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" disabled_on="on|on|on" disabled="on" /][/et_pb_column][et_pb_column type="1_3"][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads/2019/01/Gustav-Fransson6.jpg" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" custom_margin="||21px|" disabled_on="on|on|on" disabled="on" /][et_pb_text admin_label="Namn och title" _builder_version="3.0.89" background_layout="light" module_class="gen-single-ingress-module" custom_margin="||40px|" disabled_on="on|on|on" disabled="on"]

Gustav Fransson

Portfolio Manager of Coeli Nordic Corporate Bond Fund

[/et_pb_text][et_pb_image _builder_version="3.0.89" src="https://coeli.com/wp-content/uploads/2018/10/Alexander-Larsson-Vahlman.jpg" show_in_lightbox="off" url_new_window="off" use_overlay="off" always_center_on_mobile="on" force_fullwidth="off" show_bottom_space="on" custom_margin="||21px|" disabled_on="on|on|on" disabled="on" /][et_pb_text admin_label="Namn och title" _builder_version="3.0.89" background_layout="light" module_class="gen-single-ingress-module" custom_margin="||40px|" disabled_on="on|on|on" disabled="on"]

Alexander Wahlman

Senior Analyst

[/et_pb_text][et_pb_text admin_label="Fund Overview" _builder_version="3.0.89" background_layout="light" custom_margin="||20px|" module_class="gen-trustee-single-table"]

Fund Overview

| Inception Date | 2017-12-20 |

| Investment management fee (share class I SEK) | 1.00% p.a + 20% Performance fee (OMRX T-Bill Index) |

| Performance Fee. Yes | 20% |

| Risk category | 5 of 7 |

[/et_pb_text][et_pb_text admin_label="Top Holdings (%)" _builder_version="3.0.89" background_layout="light" custom_margin="||20px|" module_class="gen-trustee-single-table" disabled_on="on|on|on" disabled="on"]

Top Holdings (%)

| LANSBK 1.25% 18-17.09.25 | 4.1% |

| NORDEA HYP 1.0% 19-17.09.25 | 4.1% |

| SWEDBK 1.0% 19-18.06.25 | 4.1% |

| WHITE MOUNT FRN 17-22.09.47 | 3.9% |

| B2 HOLDING FRN 19-28.05.24 | 2.9% |

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built="1" fullwidth="off" specialty="off" _builder_version="3.0.89" module_class="gen-trustee-single-yield-section gen-pattern-section" custom_padding="0px|||"][et_pb_row _builder_version="3.0.89" custom_padding="||53px|"][et_pb_column type="4_4"][et_pb_text admin_label="VIKTIG INFORMATION" _builder_version="3.0.89" background_layout="light" module_class="gen-trustee-single-warning-blurb"]

IMPORTANT INFORMATION. This is a marketing communication.

Before making any final investment decisions, please refer to the prospectus of Coeli SICAV II, its Annual Report, and the KIID of the relevant Sub-Fund. Relevant information documents are available in English at coeli.com. A summary of investor rights will be available at https://coeli.com/regulatory-information-coeli-asset-management-ab/.

Past performance is not a guarantee of future returns. The price of the investment may go up or down and an investor may not get back the amount originally invested.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]